Management of risks. project risks A project risk is an uncertain event or condition that, if it occurs, will be positive. Project Risk Management Project Risk Management Planning

Project risk management

1. The concept and essence of project risks

When analyzing production investments, the problem of uncertainty of costs, returns, risk measurement and its impact on investment results arises. It is necessary to distinguish between the concepts of "risk" and "uncertainty".

Uncertainty implies the presence of factors under which the results of an action are not deterministic, and the degree of possible influence of these factors on the results is unknown; this is the incompleteness or inaccuracy of information about the conditions for the implementation of the project. Uncertainty factors are divided into external and internal. External factors - legislation, market reaction to manufactured products, actions of competitors; internal - the competence of the personnel of the enterprise, the error in determining the characteristics of the project, etc.

Risk is a potential, quantifiable possibility of loss. Project risk is the degree of danger to the successful implementation of the project. The concept of risk characterizes the uncertainty associated with the possibility of adverse situations and consequences during the implementation of the project, while highlighting cases of objective and subjective probabilities.

The concepts of "uncertainty" and "randomness" should also not be confused. The concept of "randomness" is narrower, it is used when there are large statistics and for each of the possible combinations of costs and results of the project, the probabilities of their implementation are determined. The concept of "uncertainty" is broader, in addition to "probabilistic", there may be other types of uncertainty. Risk occurs when some action can lead to several mutually exclusive outcomes with a known distribution of their probabilities. If such a distribution is unknown, then the corresponding situation is considered as uncertainty.

Uncertainty is not the absence of any information about the conditions for the implementation of the project, but the incompleteness and inaccuracy of the information available. Uncertainty factors must be taken into account when preparing the initial information for the development of the project, when evaluating the results of its implementation, when adjusting the implementation based on the incoming new information.

The basis of the risk of real investment of an enterprise is the so-called project risks, i.e. risks associated with the implementation of real investment projects of the enterprise. In the system of indicators for evaluating such projects, the risk level ranks third in importance, complementing such indicators as the volume of investment costs and the level of net investment profit (net cash flow).

Under the risk of a real investment project (project risk) is understood the probability of occurrence of adverse financial consequences in the form of loss of expected income in situations of uncertainty of its implementation.

The risk of a real investment project is one of the most complex concepts related to the investment activity of an enterprise. This risk has the following main features:

integrated character. The risk of a real investment project is a cumulative concept that integrates numerous types of specific investment risks. Only on the basis of an assessment of these specific types of risk can the total risk level of an investment project be determined.

Objectivity of manifestation. Project risk is an objective phenomenon in the functioning of any enterprise that makes real investment. It accompanies the implementation of almost all types of real investment projects, in whatever form they are implemented. Although a number of project risk parameters depend on subjective management decisions reflected in the process of preparing specific real investment projects, its objective nature remains unchanged.

The difference in the species structure at different stages of the implementation of a real investment project. As a rule, each stage of the process of implementing a real investment project has its own specific types of project risks. Therefore, the assessment of the total level of project risk is usually carried out for individual stages of the investment process.

High level of association with commercial risk. Investment income on the implemented project is formed, as a rule, at the post-investment phase, i.e. during the operation of the enterprise. Accordingly, the formation of a positive cash flow for an investment project occurs directly in the commodity market, i.e. is directly related to the efficiency and risk of the commercial activities of the enterprise. This determines the high degree of interrelation between the project risk and the commercial risk of the enterprise.

High dependence on the duration of the project life cycle, the time factor has a significant impact on the overall level of project risk, determining the various uncertainties of the consequences. For short-term investment projects, the determinability of external and internal factors makes it possible to choose the parameters for their implementation that generate the lowest level of risk. At the same time, for long-term investment projects, the indeterminacy of many factors and, accordingly, the uncertainty of the results of their implementation increases. The dependence of the overall level of project risk on the duration of the project life cycle is direct.

A high level of variability in the risk level for projects of the same type. The level of project risk inherent in the implementation of even the same type of real investment projects of the same enterprise is not unchanged. It varies significantly under the influence of numerous objective and subjective factors that are in constant dynamics. Therefore, each real investment project requires an individual assessment of the level of risk in the specific conditions of its implementation.

Lack of sufficient information base to assess the level of risk. The uniqueness of the parameters of each real investment project and the conditions for its implementation does not allow the enterprise to generate a sufficient amount of information that allows the use of economic, statistical, analog and some other methods for assessing the level of project risk in a wide range. The search for the necessary information to calculate this indicator is associated with the implementation of additional financial costs for the preparation and evaluation of alternative real investment projects.

Lack of reliable market indicators used to assess the level of risk. If in the process of financial investment an enterprise can use a system of stock market indicators (such indicators are developed in each country and their dynamics is reflected over a fairly long period), there are no such indicators for segments of the investment market associated with real investment. This reduces the ability to assess market factors in calculating the level of project risks.

Subjectivity of the assessment. Despite the objective nature of project risk as an economic phenomenon, its main estimated indicator - the level of risk - is subjective. This subjectivity, i.e. the unequal assessment of this objective phenomenon at specific enterprises is determined by the difference in the completeness and reliability of the information base used, the qualifications of investment managers, their experience in the field of risk management, and other factors.

Thus, investments in any project are associated with a certain risk, which is reflected in the interest rate: the project may fail, i.e. turn out to be unrealized, ineffective or less effective than expected. The risk is related to the fact that the income from the project is a random, and not a deterministic value (ie, unknown at the time of the decision to invest), as well as the amount of losses. When analyzing an investment project, one should take into account risk factors, identify as many types of risk as possible and try to minimize the overall risk of the project.

2. Classification of project risks

1.Negative (loss, damage, loss).

2.Zero.

.Positive (gain, benefit, profit).

Depending on the event, risks can be divided into two large groups: pure and speculative. Pure risks means getting a negative or zero result. Speculative risks mean getting both positive and negative results.

The risks accompanying investment activity form an extensive portfolio of enterprise risks, which is defined by the general concept - investment risk. It seems possible to propose the following classification of investment risks (Fig. 1.):

Figure 1. - Classification of investment risks

The subject of the analysis of this work is the investment project risk (the risk associated with the implementation of a real investment project) associated with investing in innovative activities, which can be defined as the probability of adverse financial consequences in the form of loss of all or part of the expected investment income from the implementation of a particular innovative activity. project in a situation of uncertainty of the conditions for its implementation.

The project risks of an enterprise are characterized by great diversity and, in order to effectively manage them, are classified according to the following main features:

By types. This classification feature of project risks is the main parameter of their differentiation in the management process. The characteristic of a particular type of risk simultaneously gives an idea of the factor that generates it, which allows you to “link” the assessment of the degree of probability of occurrence and possible financial losses for this type of project risk to the dynamics of the corresponding factor. The species diversity of project risks in their classification system is presented in the widest range. At the same time, it should be noted that the emergence of new design and construction technologies, the use of new investment products and other innovative factors will, accordingly, give rise to new types of project risks. In modern conditions, the main types of project risks include the following:

· The risk of reducing the financial stability (or the risk of imbalance in financial development) of the enterprise. This risk is generated by the imperfection of the structure of the invested capital (excessive share of borrowed funds), which generates an imbalance in the positive and negative cash flows of the enterprise on ongoing projects. As part of the project risks in terms of the degree of danger (generating the threat of bankruptcy of the enterprise), this type of risk plays a leading role.

· The risk of insolvency (or the risk of unbalanced liquidity) of the enterprise. This risk is generated by a decrease in the level of liquidity of current assets, generating an imbalance of positive and negative cash flows on an investment project over time. In terms of its financial implications, this type of risk is also among the most dangerous.

· Design risk. This risk is generated by the imperfection of the preparation of the business plan and design work on the object of the proposed investment, associated with a lack of information about the external investment environment, an incorrect assessment of the parameters of the internal investment potential, the use of outdated equipment and technology that affects its future profitability.

· construction risk. This risk is generated by the choice of insufficiently qualified contractors, the use of outdated construction technologies and materials, as well as other reasons that cause a significant excess of the stipulated terms of construction and installation works for the investment project.

· marketing risk. It characterizes the possibility of a significant reduction in the volume of sales of products provided for by the investment project, the price level and other factors leading to a decrease in operating income and profit at the stage of project operation.

· Project financing risk. This type of risk is associated with insufficient total investment resources from individual sources; an increase in the weighted average cost of capital involved in investment; imperfection of the structure of sources of formation of borrowed funds.

· inflationary risk. In an inflationary economy, it stands out as an independent type of project risks. This type of risk is characterized by the possibility of depreciation of the real cost of capital, as well as the expected income from the implementation of an investment project in inflationary conditions. Since this type of risk in modern conditions is of a permanent nature and accompanies almost all financial transactions for the implementation of a real investment project of an enterprise, constant attention is paid to it in investment management.

· interest rate risk. It consists in an unforeseen increase in the interest rate in the financial market, leading to a decrease in the level of net profit on the project. The reason for the emergence of this type of financial risk (if we eliminate its previously considered inflationary component) is a change in the investment market under the influence of government regulation, an increase or decrease in the supply of free cash resources and other factors.

· tax risk. This type of project risk has a number of manifestations: the likelihood of introducing new types of taxes and fees for the implementation of certain aspects of investment activity; the possibility of increasing the level of rates of existing taxes and fees; changing the terms and conditions for making individual tax payments; the probability of canceling the existing tax benefits in the field of real investment of the enterprise. Being unpredictable for the enterprise (this is evidenced by the modern domestic fiscal policy), it has a significant impact on the results of the project.

· Structural operational risk. This type of risk is generated by inefficient financing of current costs at the stage of project operation, causing a high proportion of fixed costs in their total amount. A high operating leverage ratio in the face of unfavorable changes in the commodity market and a decrease in the gross volume of positive cash flow from operating activities generates a significantly higher rate of decrease in the amount of net cash flow from an investment project.

· Criminogenic risk. In the field of investment activities of enterprises, it manifests itself in the form of fictitious bankruptcy declared by its partners, forgery of documents that ensure the misappropriation by third parties of monetary and other assets related to the implementation of the project, theft of certain types of assets by their own personnel, and others. Significant financial losses that, in connection with this, enterprises incur at the present stage in the implementation of an investment project, determine the allocation of criminogenic risk as an independent type of project risks.

· Other types of risks. The group of other project risks is quite extensive; in terms of the probability of occurrence or the level of financial losses, it is not as significant for enterprises as those discussed above. These include risks of natural disasters and other similar "force majeure risks", which can lead not only to the loss of expected income, but also to the loss of part of the company's assets (fixed assets, inventories), the risk of untimely settlement and cash transactions in case of project financing (associated with an unsuccessful choice of a servicing commercial bank) and others.

According to the stages of project implementation, the following groups of project risks are distinguished:

· Project risks of the pre-investment stage. These risks are associated with the choice of an investment idea, the preparation of business plans recommended for the use of investment goods, the validity of the assessment of the main performance indicators of the project.

· Project risks of the investment stage. This group includes the risks of untimely implementation of construction and installation works under the project, ineffective control over the quality of these works; inefficient financing of the project by stages of its construction; low resource support for the work performed.

· Design work of the post-investment (operational) stage. This group of risks is associated with untimely output of production to the planned design capacity, insufficient provision of production with the necessary raw materials and materials, irregular supply of raw materials and materials, low qualification of operating personnel; shortcomings in the marketing policy, etc.

According to the complexity of the study, the following groups of risks are distinguished:

· Simple project risk. It characterizes the type of project risk, which is not divided into its individual subspecies. An example of a simple project risk is inflation risk.

· Complex financial risk. It characterizes the type of project risk, which consists of a complex of its subspecies under consideration. An example of a complex project risk is the risk of the investment stage of a project.

According to the sources of occurrence, the following groups of project risks are distinguished:

· External, systematic or market risk (all of these terms define this risk as independent of the activities of the enterprise). This type of risk is typical for all participants in investment activities and all types of real investment transactions. It occurs when certain stages of the economic cycle change, the investment market situation changes, and in a number of other similar cases that the enterprise cannot influence in the course of its activities. This group of risks may include inflation risk, interest rate risk, tax risk.

· Internal, non-systematic or specific risk (all terms define this project risk as depending on the activities of a particular enterprise). It can be associated with unskilled investment management, an inefficient asset and capital structure, excessive commitment to risky (aggressive) investment operations with a high rate of return, underestimation of economic partners and other similar factors, the negative consequences of which can be largely prevented through effective project management. risks.

The division of project risks into systematic and non-systematic is one of the important initial premises of the theory of risk management.

According to the financial consequences, all risks are divided into the following groups:

· A risk that entails only economic losses. With this type of risk, the financial consequences can only be negative (loss of income or capital).

· Lost profit risk. It characterizes the situation when an enterprise, due to existing objective and subjective reasons, cannot carry out a planned investment operation (for example, if a credit rating is lowered, an enterprise cannot receive the necessary loan to form investment resources).

· A risk that entails both economic losses and additional income. In the economic literature, this type of financial risk is often called "speculative", as it is associated with the implementation of speculative (aggressive) investment operations (for example, the risk of implementing a real investment project, the profitability of which in the operational stage may be lower or higher than the calculated level).

According to the nature of manifestation in time, two groups of project risks are distinguished:

· Constant project risk. It is typical for the entire period of the investment operation and is associated with the action of constant factors. An example of such investment risk is interest rate risk.

· Temporary project risk. It characterizes the risk, which is permanent in nature, arising only at certain stages of the implementation of the investment project. An example of this type of financial risk is the risk of insolvency of an efficiently functioning enterprise.

According to the level of financial losses, project risks are divided into the following groups:

· Acceptable project risk. It characterizes the risk, the financial losses for which do not exceed the estimated amount of profit on the ongoing investment project.

· Critical project risk. It characterizes the risk, the financial losses for which do not exceed the estimated amount of gross income on the ongoing investment project.

· catastrophic project risk. It characterizes the risk, the financial losses of which are determined by the partial or complete loss of equity (this type of risk may be accompanied by the loss of borrowed capital).

If possible, project risks are divided into the following two groups:

· Forecasted project risk. It characterizes those types of risks that are associated with the cyclical development of the economy, the change in the stages of the financial market, the predictable development of competition, etc. The predictability of project risks is relative, since forecasting with a 100% result excludes the phenomenon under consideration from the category of risks. Examples of predictable project risks are inflation risk, interest rate risk and some of their other types (naturally, we are talking about risk forecasting in the short term).

· Unpredictable project risk. It characterizes the types of project risks that are characterized by complete unpredictability of manifestation. An example of such risks are the risks of a force majeure group, tax risk and some others.

According to this classification feature, project risks are also divided into regulated and unregulated within the enterprise.

If possible, project risks are also divided into two groups:

· insured project risk. These include risks that can be transferred in the order of external insurance to the relevant insurance organizations (in accordance with the nomenclature of project risks accepted by them for insurance).

· Uninsurable project risk. These include those types for which there is no offer of relevant insurance products on the insurance market.

It should be noted that the above classifications cannot be comprehensive. They are determined by the goal formulated by the classification feature. It is rather difficult to draw a clear line between individual types of project risks. A number of risks are interrelated (these risks are correlated), changes in one of them cause changes in the other. In such cases, the analyst should be guided by common sense and his understanding of the problem.

3. Analysis and assessment of project risks

Risk analysis (in investment design) - the process of studying the external and internal environment of the investment process, carried out in order to identify risks, assess their parameters, as well as predict the state of an enterprise operating under risk, after a certain point in time, by evaluating key performance indicators as random quantities. The results of the analysis are used to make decisions and to develop measures to protect against possible losses.

Project risk analysis can be divided into two complementary types: qualitative and quantitative.

Qualitative analysis can be relatively simple, its main task is to identify risk factors, stages of work during which the risk arises, i.e. identify potential risk areas, and then identify all possible risks.

Qualitative analysis implies the identification of risks inherent in the project, their description and grouping. Usually, specific risks are identified that are directly related to the implementation of the project (project), as well as force majeure, managerial, legal. For the convenience of further tracking, project risks should be taken into account by stages: initial (pre-investment), investment (construction) and operational. The result of the qualitative risk analysis stage should be a project risk map.

The description of risks at the stage of qualitative analysis does not provide information about possible losses or their probability, it serves as the basis for a quantitative risk analysis.

There are the following methods of qualitative risk analysis:

· method of expert assessments - a set of procedures aimed at identifying, ranking and qualitatively assessing the likely risks for a project based on expert opinions of people with significant experience in project activities;

· SWOT analysis - allows you to visually contrast the strengths and weaknesses of the project, its opportunities and threats based on a qualitative risk assessment;

· spiral ("rose") of risks - an illustrated ranking of risks based on qualitative assessments of risk factors;

· analogy method or conservative forecasts - a study of the accumulated experience on projects in order to calculate the probabilities of losses.

It is necessary to note one important specific feature of the qualitative analysis of project risks, which consists in its quantitative result: the process of conducting a qualitative analysis of project risks should include not only a purely descriptive, “inventory” aspect of determining certain specific types of risks of a given project, identifying possible causes of occurrence, analysis of the expected consequences of their implementation and proposals for minimizing the identified risks, but also a cost estimate of all these risk-minimizing activities for a particular project.

Conducting a quantitative analysis of project risks is a continuation of a qualitative study and assumes the existence of a certain basic option (expected profitability, cash flow calculations for the project, equipment operation time, etc.), which may change as a result of the implementation of each of the noted risks. The task of quantitative analysis is to numerically measure the degree of influence of risk factors of the project on the behavior of the efficiency criteria of the entire investment project. Thus, quantitative risk assessment is a numerical determination of the impact of individual project risks.

The quantitative risk analysis process includes the following steps:

· creation of a predictive model;

· definition of risk variables;

· determining the probability distribution of the selected variables and determining the range of possible values for each of them;

· establishing the presence or absence of correlations among risk variables;

· model runs (determining the characteristics of the resulting values as random variables);

· analysis of results (building risk levels).

Risk variables are variables that are critical to the viability of the project, i.e. even small deviations from its expected value negatively affect the project. Sensitivity and uncertainty analysis is used to select variables. Sensitivity analysis measures the response of project results to a change in one or another project variable. The disadvantage of this analysis is that it does not take into account the realism or unrealism of the expected changes in the value of the analyzed variables. In order for the results obtained from a sensitivity analysis to be meaningful, the effect of the uncertainty surrounding the variables being tested must be taken into account.

For example, a small deviation in the purchase price of a certain type of equipment per year Xis very important for project revenue, but the probability of this deviation may be small if the supplier is bound by certain terms of the contract. Therefore, the risk posed by this variable is negligible.

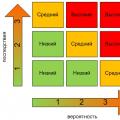

To assess the degree of acceptability of the project risk, it is necessary to allocate risk zones depending on the expected amount of losses.

Table 1. Characteristics of risk zones

Project risk zoneCharacteristicRisk-free zoneGuaranteed financial result in the amount of the estimated profitAcceptable risk zonePossible financial losses in the amount of the estimated profitArea of critical riskPossible financial losses in the amount of the estimated incomeArea of catastrophic riskPossible financial losses in the amount of equity

The assumptions made are controversial to a certain extent and not always valid for all types of risks, but on the whole quite correctly reflect the most general patterns of change in project risk and make it possible to construct a profit loss probability distribution curve, which is called the risk curve (Fig. 1.4).

The main thing in the quantitative assessment of project risk is the ability to build a risk curve and determine zones and indicators of acceptable, critical and catastrophic risks.

Figure 2. - Risk curve

Currently, the following methods of risk analysis are the most common:

1) statistical;

2)expert assessments;

)sensitivity analysis;

)assessment of financial stability and solvency;

)cost feasibility assessments;

)analysis of the consequences of risk accumulations;

)method of using analogues;

)combined method.

The statistical method consists in studying the statistics of losses and profits that have taken place in a given or similar enterprise in order to determine the likelihood of an event, to establish the magnitude of the risk. Probability means the possibility of obtaining a certain result. For example, the probability of successful promotion of a new product on the market during the year is 3/4, and failure is 1/4. The magnitude, or degree of risk, is measured by two indicators: the average expected value and the volatility (variability) of the possible outcome. The mean expected value is related to the uncertainty of the situation. It is expressed as a weighted average of all possible outcomes E(x), where the probability of each outcome BUTused as the frequency, or weight, of the corresponding value X.

The probabilistic risk assessment is mathematically sufficiently developed, but relying only on mathematical calculations in the analysis of project risks is not always sufficient, since the accuracy of the calculations largely depends on the initial information.

The method of expert assessments differs from the statistical method only in the method of collecting information to build a risk curve. This method involves the collection and study of estimates made by various specialists (of a given enterprise) regarding the probability of occurrence of various levels of losses. Expert assessment is the opinion of experts on a specific issue identified by a special methodology.

A variation of the expert method is the Delphi method. It is characterized by anonymity and controlled feedback. The anonymity of the members of the commission is ensured by their physical separation, which does not give them the opportunity to discuss the answers to the questions posed. The purpose of such separation is to avoid the "traps" of group decision-making, the dominance of the leader's opinion. After processing the result through controlled feedback, the generalized result is reported to each member of the commission. The main purpose of such an action is to allow one to get acquainted with the assessments of other members of the commission, without being subjected to pressure due to the knowledge of who specifically gave this or that assessment. After that, the assessment can be repeated.

A project sensitivity analysis consists of the following steps:

· the choice of a key indicator with respect to which the sensitivity assessment is made (net present value NPV, internal rate of return IRR etc.);

· choice of factors (inflation rate, state of the economy, etc.);

· calculation of key indicator values at different stages of project implementation (purchase of raw materials, production, sales, transportation, capital construction, etc.);

Sensitivity analysis is based on a sequential-single change in the variables tested for riskiness. At each step, only one of the variables changes its value by the predicted percentage (±5%, ±10%, ±15%, etc.), which leads to a recalculation of the final values for the project. The sequences of costs and receipts of financial resources formed in this way make it possible to determine the flows of funds of funds for each moment (or period of time), i.e. define performance indicators. Diagrams are constructed that reflect the dependence of the selected resulting indicators on the value of the initial parameters. Comparing the obtained diagrams with each other, it is possible to determine the so-called key indicators that have the greatest influence on the assessment of the profitability of the project.

Sensitivity analysis involves the following procedures:

1)The project justification model is formed in the form of a set of budgets using MS excel, project Expertany other specialized software.

2)They consider such a model as a “black box”, a system, the input of which is the initial data of the project (for example, the price of the product, the volume of expected sales, the discount interest rate, the loan rate, the estimated inflation rate, etc.), the output is “ black box" "remove" only one parameter. Most often they are the value NPV

)The justification of the project is calculated several times, using the generated model with different values of the initial data. In this case, the initial data set is formed as follows: all parameters of the initial data, except for one, are left unchanged, one parameter is considered variable, generating several of its values at once (usually five) with a certain step of relative changes. Changes, for example, can be: - 20%; - ten%; 0%; + 10%; + 20%. The model is calculated several times with different changes in the variable parameter.

)Calculate the relative growth rates of the obtained values of the net present value in relation to NPVbase variant.

)Compare the obtained values of specific growth NPVwith a specific increase in the variable parameter.

)The procedure set out in paragraphs. 3-5 are repeated for other initial parameters, taking each of them separately as variables and fixing the others.

One of the disadvantages of sensitivity analysis is the premise that each input parameter changes independently of the others. Scenario analysis helps to correct this situation when a group of interdependent indicators changes at once.

The sensitivity analysis has a serious drawback - it is not comprehensive and does not specify the likelihood of alternative projects. The sensitivity analysis of the investment project is based on the analysis of changes in one factor, which is a significant limitation of this method. Overcoming this problem is carried out within the framework of the method of statistical tests and the method of scenarios, which are the development of the methodology of sensitivity analysis.

analogy method. When analyzing the risk of a new project, data on the impact of adverse risk factors on other projects can be very useful. When using analogues, databases are used on the risk of similar projects, research work of design and survey institutions, and surveys of project managers. The data obtained in this way is processed to identify dependencies in completed projects in order to take into account the potential risk in the implementation of new projects.

When using the analogy method, some caution should be exercised. Even in the most correct and well-known cases of unsuccessful completion of projects, it is very difficult to create the prerequisites for future analysis, i.e. prepare a comprehensive and realistic set of possible project failure scenarios. The fact is that most of the negative consequences are characterized by certain features.

Simulation modeling (Monte Carlo method). Recently, the method of statistical tests - the Monte Carlo method - has become popular. Simulation modeling is a targeted series of multivariate studies performed on a computer using mathematical models. This direction corresponds to the main idea of system analysis - a combination of human capabilities as a carrier of values, a generator of ideas for decision-making with formal methods that provide the possibility of using computers. Its advantage is the ability to analyze and evaluate various "scenarios" of the project and take into account different risk factors within the same approach. Different types of projects have different risk vulnerabilities, as revealed by the simulations.

These parameters are used in simulation modeling, the algorithm of which can be represented as the following sequence of steps:

1)As in the previous case, a project justification model is formed in the form of a set of budgets using project Expertor other specialized software.

2)Similar to the corresponding step in the simulation sensitivity analysis algorithm, a model is also considered as a “black box”, a system that receives project input data (for example, product price, estimated sales volume, discount interest rate, credit rate, expected level of inflation, etc.). At the output of the black box, only one parameter is “removed”. Most often they are the value NPV, which generates a project with such initial data.

)A variable factor is selected and, if necessary, the rest are fixed, but unlike the previous method, half of the model is calculated as follows. The model is “bombarded” with random numbers with a distribution law characteristic of the behavior of the initial variable parameter with other fixed values. A series of random numbers can be sequences consisting of several thousand and even tens of thousands of values simulating a change in a variable parameter, while during the sensitivity analysis such a series consisted of only five values.

)The received values of the resulting parameter are processed (for example, NPV) in order to determine the characteristics of the behavior of the resulting quantity. The asymmetry and kurtosis of the resulting parameter is determined.

)The corresponding laws of behavior of the initial parameters are compared with the law of behavior of the resulting value. Changes in the distribution parameters of the resulting parameter in relation to the parameters of the behavior of the initial factor will indicate the significance, risk level and tendency to change the resulting project parameter.

)Appropriate conclusions are drawn and a risk factor management plan is drawn up.

The disadvantage of this method is that it uses probabilistic characteristics for estimates and conclusions, which is not very convenient for direct application and does not satisfy project managers. However, despite these shortcomings, this method makes it possible to identify the risk associated with those projects in respect of which the decision will not change. It should be noted that, in general, this method is quite laborious, because it involves cyclic repetition of the same calculations according to the model many thousands of times in the process of substituting series of random numbers as initial data, due to which the method received a second name - the Monte method. Carlo. Practice shows that the use of Monte Carlo simulation is justified, first of all, for large and expensive projects.

scenario method. Scenario methods include the following steps:

· description of the whole set of possible conditions for the implementation of the project in the form of appropriate scenarios or models that take into account the system of restrictions on the values of the main technical, economic, etc. project parameters;

· transformation of the initial information about the uncertainty factors into information about the probabilities of individual implementation conditions and the corresponding performance indicators or about the intervals for their change;

· determination of project performance indicators as a whole, taking into account the uncertainty of the conditions for its implementation.

As a result of the scenario analysis, the impact on the economic efficiency of the investment project of a simultaneous change in all other project variables that characterize its cash flows is determined. The advantage of this method is that the parameter deviations are calculated taking into account their interdependencies (correlations).

When building models, it is necessary to actively engage in the collection and formalization of expert assessments, especially in relation to production and technological risks. The main advantage of using expert assessments lies in the possibility of using the experience of experts in the process of project analysis and taking into account the influence of various qualitative factors.

As a result, it is advisable to build at least three scenarios: pessimistic, optimistic, and the most probable (realistic or average). The main problem of the practical use of the scenario approach is the need to build a model of an investment project and identify the relationship between variables.

The disadvantages of the scenario approach include:

· the need for significant qualitative study of the design model, i.e. creation of several models corresponding to each scenario, including extensive preparatory work on the selection and analytical processing of information;

· insufficient uncertainty, blurring of scenario boundaries. The correctness of their construction depends on the quality of the model construction and the initial information, which significantly reduces their predictive value. When constructing estimates of the values of variables for each scenario, some voluntarism is allowed;

· the effect of a limited number of possible combinations of variables, concluded that the number of scenarios to be detailed is limited, as well as the number of variables to be varied, otherwise it is possible to obtain an excessively large amount of information, the predictive power and practical value of which is greatly reduced.

scenario The project risk assessment method has the following features that can be considered as its advantages:

· taking into account the relationship between variables and the influence of this dependence on the values of integral indicators;

· construction of various options for the implementation of the project;

In conclusion, it should be noted that the choice of specific methods for assessing the risks of real investment is determined by a number of factors:

1.Type of investment risk.

2.The completeness and reliability of the information base formed to assess the level of probability of various investment risks.

.The skill level of the investment managers who carry out the appraisal.

.The technical and software equipment of investment managers, the possibility of using modern computer technologies for such an assessment.

.The possibility of involving qualified experts in the assessment of complex investment risks, etc.

4. Methods for reducing project risks

Understanding the nature of project risk and its quantitative assessment does not always allow effective management of real investments. In this case, the ways and methods of direct impact on the level of risk are of particular importance in order to reduce it to the maximum, increase the safety and financial stability of the design company.

Actions to reduce project risk are carried out in two directions:

1.Avoidance of possible risks.

2.Reducing the impact of risk.

The first direction is to try to avoid any possible risk for the firm. The decision to abandon the risk can be made at the decision stage, as well as by abandoning some type of activity in which the enterprise is already involved. The avoidance of possible risks includes the refusal to use large amounts of borrowed capital (financial risk avoidance is achieved), the refusal to excessive use of investment assets in low-liquid forms (liquidity reduction risk avoidance). This direction of reducing the level of project risk is the simplest and most radical. It allows you to completely avoid possible losses, but also does not make it possible to receive the amount of profit that is associated with risky activities.

In order to reduce the impact of risks, there are two ways:

1.Take measures to ensure the fulfillment of contractual obligations at the stage of concluding contracts.

2.To exercise control over management decisions in the process of project implementation.

On the first path, there are several options for action:

·insurance;

· security (in the case of a loan agreement) in the form of a pledge, guarantee, surety, forfeit or retention of the debtor's property;

· step-by-step separation of the project appropriation approval process;

· investment diversification.

Options for management decisions in order to reduce project risk can be carried out by the following methods:

1.Reservation of funds to cover unforeseen expenses.

2.Loan restructuring.

Consider some of the ways to reduce project risk.

One of the most important ways to reduce project risk is diversification, for example, the distribution of an enterprise's efforts between activities, the results of which are not directly related to each other. Any investment decision related to a particular project requires the decision maker to consider the project in relation to other projects and existing activities of the enterprise. To reduce risk, it is desirable to plan the production of such goods and services, the demand for which changes in opposite directions.

The distribution of project risk among project participants is an effective way to reduce it, it is based on the partial transfer of risks to partners in individual investment situations. In this case, it is most logical to make responsible the one of the participants who has the ability to more accurately and better calculate and control the risk. The distribution of risk is taken into account when developing the financial plan of the project and is formalized in contract documents.

A possible way to reduce risk is to insure it, which essentially consists in transferring certain risks to an insurance company. When making a decision on external risk insurance, it is necessary to evaluate the effectiveness of this method of risk reduction, taking into account the following parameters:

1.The probability of an insured event occurring for a given type of project risk.

2.The degree of insurance coverage for risk, determined by the coefficient of insurance (the ratio of the sum insured to the size of the insurance valuation of the property).

.The size of the insurance tariff in comparison with its average size in the insurance market for this type of insurance.

.The amount of the insurance premium and the procedure for its payment during the insurance period, etc.

Foreign practice of insurance uses full insurance of investment projects. The conditions of Russian reality allow so far only partially insure project risks: buildings, equipment, personnel, some extreme situations.

Type of costsChange in contingencies, %Costs / duration of work of Russian contractors + 20Costs / duration of work of foreign contractors + 10Increase in direct production costs + 20Decrease in production - 20Increase in interest for a loan + 20

In addition to reserving for force majeure, it is necessary to create a system of reserves at the enterprise for optimal cash flow management. We are talking about the formation of a reserve fund, a fund for the repayment of uncollectible receivables, maintaining the optimal level of inventories and the regulatory balance of cash and their equivalents. Reservation of funds is, in fact, self-insurance (internal insurance) of the enterprise. At the same time, it should be borne in mind that insurance reserves in all their forms, although they allow you to quickly compensate for the losses incurred, however, “freeze” the use of a fairly tangible amount of investment resources. As a result, the efficiency of using the company's own capital decreases, and its dependence on external sources of financing increases.

Limiting as a way to reduce risks consists in setting by the enterprise the maximum allowable amount of funds for the performance of certain operations (or project stages), in the event of the loss of which this will not significantly affect the financial condition of the enterprise. Limitation is used by banks when issuing loans, industrial enterprises - when selling goods on credit, determining the amount of capital investments, determining the amount of borrowed funds, and also in other situations.

An important role in reducing project risks is played by the acquisition of additional information. The purpose of such an acquisition is to clarify some project parameters, increase the level of reliability and reliability of the initial information, which will reduce the likelihood of making an inefficient decision. Methods for obtaining additional information include purchasing it from other organizations, conducting an additional experiment, etc. Complete and reliable information is a special kind of commodity that you have to pay for, but these costs are repaid by obtaining significant benefits from less risky investments.

Concluding the review of the main aspects of the theory of project risk management, the following should be noted. Identification of project risks, their accounting and analysis is part of the overall system for ensuring the economic reliability of an economic entity.

Conclusion

In conclusion, the following main aspects should be noted.

Risk in a market economy accompanies any management decision. This is especially true for investment decisions, the consequences of which affect the activities of the enterprise over a long period of time.

Bibliography

1.Afonasova, A.M. Design analysis. Lectures [Electronic resource] / A.M. Afonasova. Access mode: #"justify">2. Blank, I.A. Investment management [Text]: training course / I.A. Form. - 2nd ed., corrected. and additional - K .: Elga-N, Nika-Center, 2007. - 448 p.

.Kalmykova, T.S. Investment analysis [Text] / T.S. Kalmykov. - M.: INFRA-M, 2009. - 240 p.

.Kovalev V.V. Introduction to financial management [Text] / V.V. Kovalev. - M.: Finance and statistics, 2008. - 786 p.: ill.

.Osipova, L.M. Economic evaluation of investments [Text]: guidelines / L.M. Osipov. - Kemerovo: Printing house of GU KuzGTU, 2011. - 40 p.

.Kharlamenco, E.V. Quantitative risk analysis of the investment project [Text] // E.V. Kharlamenco. - Russian entrepreneurship. - 2009. - No. 5 (1).

.Tsarev, V.V. Estimation of economic efficiency [Text] / V.V. Tsarev. - St. Petersburg: Peter, 2007. - 464 p.

project risk investment sensitivity

Tutoring

Need help learning a topic?

Our experts will advise or provide tutoring services on topics of interest to you.

Submit an application indicating the topic right now to find out about the possibility of obtaining a consultation.

Keywords: PROJECT MANAGEMENT; RISK; PROJECT LIFE CYCLE; MECHANISMS OF IMPACT; POSSIBLE RISKS; METHODOLOGY; PROJECT MANAGEMENT; RISK; PROJECT LIFE CYCLE; MECHANISMS OF ACTION; THE POTENTIAL RISKS; THE METHODOLOGY.

Annotation: The article describes possible risks in project management, gives recommendations when planning a project in order to identify all possible risks.

Today, when it comes to project management, it is unwittingly associated with the topic of possible risks. Every project, new or old, has its own life cycle. Thus, a project is born from planning, which is aimed at determining and agreeing on the best course of action to achieve the set goals of the project, taking into account all the factors of its implementation. The planning process does not end with the development and approval of the initial project plan. So, for example, there can often be changes during the course of a project. Changes most often occur within the project, but they tend to be in the external environment as well. As a result, the project is often rescheduled or the plans of the project being implemented are clarified, from this we can conclude that the planning process can exist throughout the entire life cycle of the project.

The project management methodology includes procedures, methods and tools for implementing the processes of initiating, planning, organizing execution, monitoring execution and completing the project. Project initiation is the process of project management, the result of which is the authorization of the start of the project or the next phase of its life cycle.

To achieve the goals of the project, it is necessary to create special structures that will include: the project team and the project management team. In many ways, the success of the entire project will depend on the effectiveness of such structures.

It is worth noting the possible risks that may be present along the entire life cycle of the project. As defined by the American Project Management Standard PMBOK (2004), a project risk is an uncertain event or condition that, if it occurs, has a positive or negative impact on at least one of the project objectives, such as timing, cost, content or quality. The risk can not only have negative consequences, but also positive ones, leading to an improvement in the quantitative and qualitative indicators of the characteristics of the final goals of the project being implemented. If we consider the risk as an integral part in the life cycle of the project, then an analysis of possible project risks should be carried out. Analyzes of project risks are ranked into qualitative and quantitative ones.

Qualitative risk assessment is a qualitative analysis process that requires a quick response. Such a risk assessment can determine the importance of the risk and how to respond to that risk. The availability of information on these risks will help to prioritize for different criteria and categories of risks. The use of these tools helps to partially avoid the uncertainty that often occurs in the project. During the life cycle of the project, there should be a constant reassessment of risks.

Quantitative risk assessment determines the probability of occurrence of risks. It also helps the manager or his group led by him to make the right decisions - the impact of the consequences of risks on the project. Risk assessments such as quantitative and qualitative can be used individually or together. Depends on available budget, time and need for such risk assessments.

A section in the project plan should be allocated for the results of the risk analysis, which will include a description of the risks, mechanisms of influence, measures to protect against the expected risks. Risk factors are events that may occur and have a deviating effect on the implementation of the intended project plan, or any conditions that cause uncertainty in the final result of the situation. Also, some of the events that were indicated could have been foreseen, while others could not have been predicted. If we talk about risk analysis, then it is carried out from the point of view of: the causes of occurrence, possible negative consequences, the forecast of specific measures to minimize the risk. The main results of a qualitative risk analysis are: identification of specific project risks and their causes; analysis and cost equivalent of the hypothetical consequences of the possible implementation of the noted risks; proposal of measures to minimize damage and their cost estimate. The risk that is associated with projects is characterized by the following factors: risk probability; risk event; cost, non-value factors at risk.

Application of the method of constructing a decision tree of the project. When you have a small number of variables and the smallest number of project development scenarios, you can use this method for risk analysis. The great advantage of this method is its clarity. To build a decision tree in risk analysis, sequential data collection is carried out, which includes the following steps: determining the composition and duration of the phases of the project life cycle; identification of key events that may affect the further development of the project; determining the timing of key events; formulation of all possible decisions that can be made as a result of the occurrence of each key event; determining the probability of making each decision; determination of the cost of each stage of the project. By building a decision tree, you can understand the likelihood of each scenario.

To maximize the study of possible risks in the project, you can use the Monte Carlo simulation method. It is a combination of sensitivity analysis and scenario analysis methods. The result of this method is the probability of possible outcomes of the project. However, there is difficulty in applying this method due to variables that are incorrectly specified and may lead to inaccurate conclusions.

Speaking about risk reduction methods, we can say that all methods that allow minimizing project risks can be divided into three groups.

Risk distribution allows you to rank risks between project participants. Such distribution among project participants is an effective way. This distribution of risks between project participants increases the reliability of achieving the result. It is most correct to make a person responsible for a specific type of risk, who can qualitatively control the risk given to him.

Reserve funds to cover sudden (unplanned) expenses. If the project participants cannot ensure the implementation of the project before the risk event themselves, then it is necessary to carry out risk insurance. Risk insurance is the transfer of certain risks to an insurance company.

The effectiveness of methods for reducing all risks is determined using a certain algorithm: considering the risk that is of the greatest importance for the project; the overspending of these funds is determined taking into account the probability of an adverse event; determination of cost overruns, taking into account the likelihood of an adverse event; a list of possible measures is determined that are aimed at reducing the likelihood and danger of a risk event; additional costs for the implementation of the proposed measures are determined; comparison of the required costs for the implementation of the proposed activities with the possible cost overrun due to the occurrence of a risk event; a decision is made on the implementation or refusal of anti-risk measures; the process of compiling the probability and consequences of risk events with the costs of measures to reduce them is repeated for the next most important risk.

A comprehensive study of all kinds of risks at the initial stage of the project using these approaches and methods is undertaken not only in risk analysis. Thanks to such studies, the conclusions are of help at the project implementation stage, since the analysis of such project risks should not be limited to facts. Certain steps are taken in the risk management process, such as: identifying perceived risks; analysis and assessment of project risks; choice of risk management choices; application of selected methods; evaluation of risk management results. Risk management is carried out at all stages of the project life cycle through monitoring, control and necessary corrective actions by the project manager.

When characterizing aspects of project risk management methods, it is necessary to highlight a clear focus that allows not only to identify risk factors, but also to model the process of project implementation. Assess the possible likelihood of certain consequences of an unfavorable situation that have arisen. Propose measures that would compensate for risks, select methods, track the actual dynamics of the project, and adjust the direction in order to improve. Also, at the initial stage of project planning, its inception, it is necessary to apply all methods to the development of such a project. In order to minimize all kinds of risks that may arise during the implementation phase, and after implementation, various risk modeling activities (such as brainstorming, system analysis) should be applied. The goal of project risk management is not only to deepen the analysis of the project, but also to increase the effectiveness of decisions. The role of the main executor of all methods and decision-making related to risk management falls on the shoulders of the project manager or the team with his participation.

Thus, risk management methods (project risks) can be a powerful tool for the effective implementation of the projects themselves at all levels of management.

Bibliography

- Burkov V.N., Novikov D.A. How to manage projects. // - M., 2004. - S.56-57.

- Bagyuli F. Project management. // -M.: FAIR-PRESS, 2004. - P.155.

- Mazur I.I. Project management: textbook. manual for universities "Management org." // I.I. Mazur, V.D. Shapiro, under common. ed. I.I. Masuria. -2nd ed. — M.: Omega-L, 2004. S.433-434.

- As shown by the competition of business plans, held by the company "Corporate Finance" and the journal "Financial Director", the most common mistake of enterprises planning the implementation of investment projects is insufficient study of risks that may affect the profitability of projects 1 . Since such errors can lead to incorrect investment decisions and significant losses, it is very important to identify and assess all project risks in a timely manner.

As a rule, project risks are understood as the expected deterioration in the final indicators of the project's effectiveness, arising under the influence of uncertainty. In quantitative terms, risk is usually defined as a change in the numerical indicators of the project: net present value (NPV), internal rate of return (IRR) and payback period (PB) 2 .

At the moment, there is no single classification of enterprise project risks. However, the following main risks inherent in almost all projects can be distinguished: marketing risk, the risk of non-compliance with the project schedule, the risk of exceeding the project budget, as well as general economic risks.

Next, we will consider the risks of the project using the example of a jewelry factory that decided to launch a new product on the market - gold chains 3 . Imported equipment is purchased for the production of the product. It will be installed in the premises of the enterprise, which is planned to be built. The price of the main raw material - gold - is determined in US dollars based on the results of trading on the London Metal Exchange. The planned sales volume is 15 kg per month. The products are supposed to be sold both through own stores (30%), some of which are located in large shopping centers, and through dealers (70%). Sales have a pronounced seasonality with a surge in December and a decrease in sales in April-May. The launch of the equipment should take place before the winter peak of sales. The project implementation period is five years. Managers consider net present value (NPV) as the main measure of project performance. Estimated planned NPV is $1,765 thousand.

Main types of project risks

Marketing risk

Marketing risk is the risk of not receiving profits as a result of a decrease in the volume of sales or the price of a product. This risk is one of the most significant for most investment projects. The reason for its occurrence may be the rejection of the new product by the market or an overly optimistic estimate of future sales. Errors in planning a marketing strategy arise mainly due to insufficient understanding of the needs of the market: incorrect product positioning, incorrect assessment of market competitiveness or incorrect pricing. Also, errors in the promotion policy can lead to risk, for example, choosing the wrong promotion method, insufficient promotion budget, etc.

Yes, in our example 30% of the chains are planned to be sold independently, and 70% - through dealers. If the sales structure turns out to be different, for example, 20% - through stores and 80% - through dealers, for which lower prices are set, then the company will not receive the originally planned profit and, as a result, project performance will deteriorate. This situation can be avoided primarily through a comprehensive assessment of the market environment by the marketing department.

External factors can also influence sales growth rates. For example, some of the company's own stores in case in question opens in new shopping centers, respectively, the volume of sales in them will depend on the degree of "promotion" of these centers. Therefore, to reduce the risk in the lease agreement, it is necessary to establish qualitative parameters. Thus, the rental rate may depend on the fulfillment by the shopping center of the schedule for launching retail space, ensuring the transportation of customers to the point of sale, the timely construction of parking lots, the launch of entertainment centers, etc.

Risks of non-compliance with the schedule and exceeding the project budget

The reasons for the occurrence of such risks can be objective (for example, a change in customs legislation at the time of customs clearance of equipment and, as a result, delay in cargo) and subjective (for example, insufficient study and inconsistency in the implementation of the project). The risk of non-compliance with the project schedule leads to an increase in the payback period, both directly and due to lost revenue. AT our case this risk will be great: if the company does not have time to start selling a new product before the end of the winter peak of sales, then it will suffer big losses.

Similarly, overall project performance is affected by the risk of over budget.

- Determination of the real time and budget of the project

For a more accurate assessment of the project time and budget, there are special methods, in particular, the PERT analysis method ( Program Evaluation and Review Technique), developed in the 1960s by the US Navy and NASA to estimate the construction time of the Polaris ballistic missile. The methodology turned out to be effective and was subsequently used to assess not only the timing, but also the resources of the project. Currently, PERT analysis is one of the most popular and simple techniques.

The meaning of this method is that when preparing a project, three estimates of the implementation period (project cost) are given - optimistic, pessimistic and most probable. After that, the expected values are calculated using the following formula: Expected Time (Cost) = (Optimistic Time (Cost) + 4 x Most Likely Time (Cost) + Pessimistic Time (Cost)) : 6. Coefficients 4 and 6 are obtained empirically based on the statistical data of a large number of projects. The result of the calculation is used later as the basis for obtaining the rest of the project indicators. However, it should be noted that the PERT analysis design is only effective if you can justify the values of all three estimates.

If the work is performed by external contractors, then as a way to minimize these risks, special conditions can be stipulated in the contract. So, in our example, when preparing a project, work is planned to build a room and install equipment, performed by an external counterparty. The duration of these works should be three months, the cost - 500 thousand US dollars. After completion of the work, the company plans to receive additional revenue from the production of chains in the amount of 120 thousand US dollars per month at a profitability of 25%. If the supplier causes the repair and installation time to increase by, say, one month, then the company will lose $30,000 (1 x 120 x 25%) in profit. To avoid this, the contract defines sanctions in the amount of 6% of the contract value for one month of delay due to the fault of the contractor, that is, 30 thousand US dollars (500 thousand x 6%). Thus, the size of the sanctions is equal to the possible loss.

When implementing a project only on its own, it is much more difficult to minimize risks, while the amount of losses may increase.

In our example if you install the equipment on your own, in case of a delay of one month, the loss of profit will also amount to 30 thousand US dollars. However, additional labor costs for employees during this month should be taken into account. Let in our example, such costs amount to 7 thousand US dollars. Thus, the total losses of the company will be equal to 37 thousand US dollars, and the payback period of the project will increase by 1.23 months (1 month + 7 thousand US dollars: (120 thousand US dollars x 25%)). Therefore, in this case, a more accurate assessment of the duration and cost of work, as well as effective management of the project implementation process and its constant monitoring, are required.

General economic risks

General economic risks include risks associated with factors external to the enterprise, for example, risks of changes in exchange rates and interest rates, an increase or decrease in inflation. Such risks also include the risk of increased competition in the industry due to the overall development of the economy in the country and the risk of new players entering the market. It should be noted that this type of risk is possible both for individual projects and for the company as a whole.

In our example the most significant is the currency risk. When calculating a project, all cash flows are often given in a stable currency, such as US dollars. However, to better account for currency risk, cash flows should be calculated in the currency in which the payment is made. Otherwise, you can get an underestimation of the currency risk, since the fluctuation in exchange rates will not be taken into account. For example, if both inflows and investments are calculated in the same currency, and the dollar exchange rate rises, but the ruble price of the product does not change, then in fact we will receive less revenue in dollar terms. The use of different currencies for the calculation will take this factor into account, but one currency will not. This is especially true in our case, when all capital investments for the repair of the building and the purchase of equipment are made in foreign currency, and the proceeds from the sale of products - in rubles.

Project risk analysis

The procedure for assessing and analyzing project risks can be represented as a diagram (see Fig. 1).

Risk assessment is carried out during the project planning process and includes qualitative and quantitative analysis. If, based on the results of the assessment, the project is accepted for execution, then the enterprise faces the task of managing the identified risks. According to the results of the project implementation, statistics are accumulated, which allows in the future to more accurately identify risks and work with them. If the uncertainty of the project is too high, then it can be sent for revision, after which the risks are reassessed.

The procedure for managing project risks, as well as collecting and using statistical information in a particular situation, depends on the specifics of the company and the project being implemented and is not considered in this article.

Let us consider the qualitative and quantitative assessment of project risks in more detail.

Qualitative risk analysis

The result of a qualitative risk analysis is a description of the uncertainties inherent in the project, the reasons that cause them, and, as a result, the risks of the project. For the description, it is convenient to use specially designed logical maps - a list of questions that help identify existing risks. These maps can be developed both independently and with the help of consultants (see Fig. 2).

As a result, a list of risks to which the project is exposed will be formed. Further, they must be ranked according to the degree of importance and the magnitude of possible losses, and the main risks should be analyzed using quantitative methods for a more accurate assessment of each of them.

In our example analysts identified the following main risks: failure to achieve planned sales volumes due to both their lower physical volume (in physical terms) and lower prices, as well as a decrease in profit margins due to rising raw material prices.

Quantitative risk analysis

Quantitative risk analysis is necessary in order to assess how the most significant risk factors can affect the performance of an investment project. The analysis allows you to find out, for example, whether a small change in sales volume will lead to a significant loss of profit or whether the project will be profitable even if 40% of the planned sales volume is realized.

There are several main methods for conducting such an analysis: analysis of the influence of individual factors (sensitivity analysis), analysis of the influence of a complex of factors (scenario analysis) and simulation modeling (Monte Carlo method). Let's consider each of them in more detail, using the indicators of our example.

Sensitivity analysis. This is a standard method of quantitative analysis, which consists in changing the values of critical parameters ( in our case physical volume of sales, cost and sales price), substituting them into the financial model of the project and calculating project performance indicators for each such change. Sensitivity analysis can be implemented using both specialized software packages (Project Expert, Alt-Invest) and Excel. Calculations for analysis are most conveniently presented in the form of a table (see Table 1).

Such a calculation is carried out for all critical factors of the project. The degree of their impact on the final effectiveness of the project (in this case, on NPV) is more convenient to show on the graph (see Fig. 3).

Thus, the result of the project under consideration is most strongly influenced by the selling price, then the cost of production and, finally, the physical volume of sales.

Although the selling price has a large influence on NPV, the probability of its fluctuation can be very low, therefore, changes in this factor will pose little risk. To determine this probability, the so-called "probability tree" is used. First, based on expert opinions, the probability of the first level is determined - the probability that the real price will change, that is, it will become more, less or equal to the planned one ( in our case these probabilities are equal to 30, 30 and 40%), and then the probability of the second level is the probability of deviation by a certain amount. In our example the reasoning is as follows: if the price still turns out to be less than the planned one, then with a probability of 60% the deviation will be no more than -10%, with a probability of 30% - from -10 to -20% and with a probability of 10% - from -20 to -30% . Deviations in the positive direction are analyzed in a similar way. Deviations of more than 30% in any direction were considered impossible by the experts.

The final probability of the sales price deviation from the planned value is calculated by multiplying the probabilities of the first and second levels, so the final probability of a price reduction by 20% is quite small - 9% (30% x 30%) (see Table 2).

Total risk by NPV in our example is calculated as the sum of the products of the final probability and the risk value for each deviation and is equal to $6.63 thousand(1700 x 0.03 + 1123 x 0.09 + 559 x 0.18 - 550 x 0.18 - 1092 x 0.09 - 1626 x 0.03). Then the expected value of NPV, adjusted for the risk associated with a change in the selling price, will be equal to 1758 thousand USD(1765 (target NPV) - 6.63 (expected risk)).

Thus, the risk of changes in the selling price reduces the NPV of the project by 6.63 thousand US dollars. As a result of a similar analysis of two other critical factors, it turned out that the most dangerous is the risk of changes in the physical volume of sales: the expected value of this risk was 202 thousand US dollars, and the expected value of the risk of changes in the cost of 123 thousand US dollars. It turns out that a change in the retail price is not the most important risk for the project under consideration and can be neglected, focusing on managing and preventing other risks.

Sensitivity analysis is very clear, but its main drawback is that the influence of only one of the factors is analyzed, and the rest are considered unchanged. In practice, several indicators usually change at once. Scenario analysis helps to assess such a situation and adjust the NPV of the project for the amount of risk.

Scenario analysis. To begin with, it is necessary to determine the list of critical factors that will change simultaneously. To do this, using the results of the sensitivity analysis, you can select 2-4 factors that have the greatest impact on the outcome of the project. Considering more factors at the same time does not make sense, since this only complicates the calculations.

Three scenarios are usually considered: optimistic, pessimistic and most probable, but if necessary, their number can be increased. In each of the scenarios, the corresponding values of the selected factors are fixed, after which the project's performance indicators are calculated. The results are tabulated (see Table 3).

As with sensitivity analysis, each scenario is assigned a probability based on expert judgment. The data of each scenario is substituted into the main financial model of the project, and the expected NPV values and risk values are determined. The magnitude of the probabilities, as in the previous case, must be justified.

The expected value of NPV in this case will be equal to 1572 thousand USD(-1637 x 0.2 + 3390 x 0.3 + 1765 x 0.5). Thus, unlike the previous stage of the analysis, we received one more accurate comprehensive assessment of the effectiveness, which will be used in further decisions on the project. It should be taken into account that a large gap between the planned and estimated NPV values indicates a high project uncertainty. There may be additional risk factors in the project that need to be considered.

Simulation modeling. In the case when exact estimates of the parameters (for example, 90, 110 and 80%, as in scenario analysis) cannot be set, and analysts can only determine the intervals of possible fluctuations of the indicator, the Monte Carlo simulation method is used. Most often, such an analysis is carried out to identify currency risks (fluctuations in the exchange rate during the year), as well as risks of fluctuations in interest rates, macroeconomic risks and others.