Calculation of the average salary. Calculation of temporary disability benefits

annotation

New 20th edition bestselling book "Wages"- For 20 years, thousands of accountants have been using this book every day in their work! The most full information about settlements with employees, a huge number of practical digital examples for all occasions, including the most confusing ones.

The issues of organizing wages are always relevant and difficult: the desires and interests of employees are limited by the employer's capabilities, who have to settle accounts not only with employees, but also with the budget and extra-budgetary funds. Errors in calculations, registration and payment wages, in calculating taxes and insurance premiums, they lead not only to claims on the part of employees, but also to sanctions on the part of labor inspectorates, tax authorities, Pension Fund and FSS RF. In the book, all payments in favor of employees are clearly classified and considered not only from the point of view of labor legislation, but also taking into account the provisions Tax Code Russian Federation and laws on pension and social insurance. Controversial issues are identified, an analysis of various approaches to their solution is carried out, a reasoned assessment of their compliance with the current legislation and specific recommendations are given. This will allow readers to consciously choose the best option reducing the risk of errors leading to labor and tax disputes. In edition changes in legislation that came into force in 2017 were taken into account, including complete information on the new rules for paying insurance premiums and submitting reports to tax authorities.

The book is addressed to accountants of small, medium and large organizations of all forms of ownership, economists, auditors, as well as heads of organizations.

ATTENTION! The website of the ICG Publishing House www.icgr.ru will provide online support for the relevance of the book "Salary in 2017" throughout 2017. On a special page, the author will post information about the changes affecting the issues discussed in the book. Access to this page will be open to all readers. Visit the website of the IC Publishing House throughout the year and be aware of all the changes.

I ordered this book in 2016, I really like it detailed description types of charges with examples. I am delighted! I don’t regret that I got it.

I bought the book like a dark horse, but I was very pleased !!! a clear explanation from the basics of all the intricacies of payroll and everything else related to it. And most importantly, with a cursory review, I noticed that the book was not written in dry language. normative documents- but with a huge number of explanations and explanations that will be useful specifically to employers for the correct calculation and optimization of costs, which is very important at the present time. I am delighted!!!

I highly recommend the book to anyone who has anything to do with payroll, regardless of the degree of your knowledge of the subject. For beginners, the book will be a textbook, for experienced accountants - a guide to complex and controversial issues of payroll.

I myself have been using Vorobyeva's books for a very long time. I have the previous book from 2013. There are differences, and for the better.

For example, I really liked how now the book deals with the situation with payment for work on weekends and holidays. I recommend that you familiarize yourself with the specialists of Rostrud and the Ministry of Labor (so as not to issue stupid letters on this topic).

In terms of print quality, it is traditional for such books "gray paper". But this does not detract from the value of the book. In addition, this book has to be periodically updated (appears new information, or the old one is presented in a more accessible and convenient form).

From May 1, 2018, the minimum wage will be 11,163 rubles (+ 17.6%), i.e. will be equated to the federal cost of living for workers. Vladimir Putin announced this at a meeting with the workers of the Tver Carriage Works.

Russian President Vladimir Putin signed a law to increase minimum size wages (minimum wage). According to him, the minimum wage from July 1, 2017 will be increased by 4%, from 7,500 rubles. up to RUB 7800 per month.

Table of regional minimum wages in 2017 by constituent entities of Russia. More precisely, this is called the Minimum Wage in the Regions (MW). Not all regions have raised the minimum wage level above the federal level.

In fact, the salary of an employee, handed out, may be lower than the minimum wage in the region, since the minimum wage is calculated from the accrued salary, i.e. before personal income tax withholding. Accordingly, with an accrued salary of 1 minimum wage (7,800 rubles), the amount paid to an employee by hand is reduced by the amount of personal income tax. Also, the calculation of the sick leave may not be lower than the calculation based on the local minimum wage.

|

|

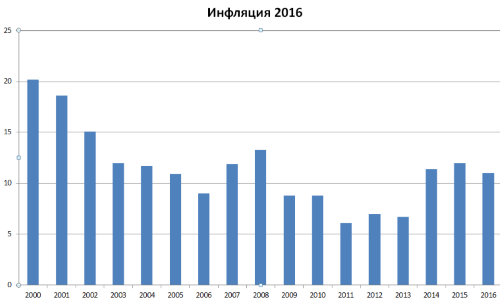

Rice. Inflation dynamics in Russia 2000-2016 |

You can find out about the size of the minimum wage and about its changes in 2016 in the article

Salary is the employee's remuneration for work. Her employer must pay his subordinates in accordance with labor legislation RF. Earnings are calculated monthly, and issued twice during this period in the form of remuneration for the first half of the month (advance) and full payment.

The size of the salary, the list of additional payments, the procedure and conditions for their receipt are established by the employer independently and fixed in the regulatory documentation.

The employee has the right to know how the remuneration is accrued to him, what components it consists of.

The head of the company and the chief accountant are responsible for the accrual and timeliness of payment of earnings.

Definition of concepts

Salary is a set amount of money that an employee receives from his employer for completing certain work... The functions performed by the employee are prescribed in the employment agreement or are negotiated orally.

The obligatory part of wages is called basic earnings. It is approved in advance and communicated to the worker by signing an employment agreement. This can be a salary, a wage rate, or a piece rate.

The basic salary includes various additional payments and allowances (for length of service, for overtime work, etc.), payment for downtime for reasons beyond the control of the employee.

Additional salary includes non-compulsory payments that are assigned at the initiative of the management. These are incentives for over-standard work, benefits, payments for working conditions, and others.

These include:

- vacation pay;

- severance pay;

- payment for unworked time provided for by the Labor Code of the Russian Federation;

- payment for breaks in the work of nursing women, etc.

The employer is obliged to conclude an employment agreement with each employee. Its content must comply with Art. 135 of the Labor Code of the Russian Federation. The document covers all issues related to remuneration: the size of the salary (rate, tariff), the procedure and conditions for receiving additional payments, working conditions, etc.

According to Art. 136 TC, earnings must be paid to staff at least twice a month. The company determines the specific dates of payments independently and fixes it in the local normative act: Collective agreement, Regulations or Rules of the order of work.

By Russian legislation full payment for the month must be made by the 15th day of the next, and the advance payment must be made by the end of the current month. The interval between two payments cannot exceed 15 days. For example, if the day of advance payment in the organization is the 25th, then earnings for the entire period must be issued on the 10th of the next month.

The employer is obliged to transfer the vacation 3 calendar days before the date of the start of the vacation. If the maximum day of payment coincided with a weekend or a holiday, then it must be made the day before.

Earnings are divided into:

Now employers have the right to independently choose the system and form of payment for work, the mode of work and rest, the list of additional payments and allowances. The main condition is compliance with the labor legislation of the Russian Federation.

Minimum wage

The salary of a full-time employee per month must not be less than the minimum wage established by the Government.

This value in Russia is used for the following purposes:

- regulates wages;

- participates in the formation of pensions;

- used to calculate benefits;

- determines the amount of taxes, fines and other payments that depend on the minimum wage and are calculated in accordance with the law.

The minimum wage is regularly reviewed and increased. Its size depends on the inflation rate, the cost of the consumer basket and other economic factors. Now it is equal to 7,500 rubles.

An increase in the minimum wage leads to an increase in earnings, employers' contributions to the budget and funds, and an increase in prices.

The size of the minimum wage is set at the federal level, the regional authorities are entitled to increase this indicator.

According to Art. 133 TC sources of financing for minimum wages are own funds companies, and for state employees - the budget of the corresponding level (federal, regional or local).

The federal minimum wage is legally binding. It is approved by the Federal Assembly and signed by the President.

At the regional level, the indicator is established by a tripartite agreement between:

- the government or administration of the entity;

- by a trade union or other body from workers;

- the union of industrialists and entrepreneurs from employers.

The agreement is published in the regional media. Within a month, employers have the right to express their disagreement with him. For this, an application is drawn up to the administration.

In accordance with Article 129 of the Labor Code, the components of the minimum wage include:

- remuneration for work, taking into account the professionalism of the employee. The volume of work, their complexity and working conditions;

- additional payment for special working conditions (northern allowance, harmfulness of production, etc.);

- bonus, allowance, incentive payment.

If an employee is busy additionally, for example, a teacher works for 1.5 times, his minimum wage cannot be less than 1.5 minimum wages. Work is paid additionally on holidays and weekends, overtime and night hours.

The amount of earnings accrued to an employee for a month cannot be less than the minimum wage, he will receive the amount minus deductions in his hands, so it will be below the minimum value.

For wages below the minimum wage, administrative liability is provided. Executive will be fined in the amount from 1 to 5 thousand rubles, a legal entity - from 30 to 50 thousand rubles, the activities of the company may be suspended for a period of up to three months.

Official and unofficial salary

The salary is considered official, which is indicated in the employment agreement when hiring a worker and in the corresponding order.

It is also reflected in the local documents of the company:

- Collective agreement;

- Regulations on remuneration;

- Regulations on prizes;

- etc.

Before issuing it, each employee receives a payroll, which reflects all accruals, deductions, interim payments made to him, and the amount to be issued. By this document a worker can independently calculate his earnings, and discuss any incomprehensible or controversial issue with management or accounting.

The official salary is per-hour and piece-rate. In the first case, it is based on the salary, all additional payments are calculated from it. Piecework wages depend on the production rate.

Salary consists of several components.

For example, for state employees, these include:

- salary;

- incentive payments (for seniority, for intensity, etc.);

- compensation payments(for travel, food, harm, young professionals, etc.);

- awards;

- other surcharges.

The earnings include payment for vacation, sick leave, business trips, and other charges. When a citizen is hired, an accountant opens a personal card for him, in which he enters personal data and all information about earnings established in the organization for a specialist in this position.

From the accrued amount, employees are paid a monthly advance in the amount of not more than 50% of it. The rest of the amount is included in the final earnings. It is calculated on the last day of the month when all charges are made.

Personal income tax is withheld from the total accrued earnings, which is usually 13%. Alimony and other amounts based on court decisions can also be deducted. On wage day, the employee will receive the amount of accruals minus deductions and the advance issued earlier.

In the middle of the month, other interim payments can be made, for example, vacation pay, then these amounts are also deducted from the accrued at the end of the period.

Unofficial earnings include payments to staff that are not reflected in any employer's documents. Such machinations are illegal. Upon discovery of this fact, responsibility lies with both parties to the transaction.

Often, a company pays an employee a part of the salary officially, and gives the rest of the money, by verbal agreement, in the form of a “gray” salary.

Employers use this approach to save money on taxes or to pay for labor to persons who are not on the staff of the enterprise.

Some joint stock companies use their own scheme of informal payments. They sell to each worker a few shares, which they promise to return upon dismissal. Under labor agreements, staff officially pay the minimum wage. The rest of the earnings are given, bypassing taxation, under the guise of dividends.

Tax authorities carefully check the documentation of shareholders' meetings, data of employment contracts, shares of each employee and the frequency of payments. Often during the audit, a lot of errors and inaccuracies are revealed, which help to reveal the fact of unofficial calculations.

It is beneficial for employees to receive money in an envelope. These amounts are not subject to personal income tax and alimony is not withheld from them.

There are many disadvantages in unofficial earnings:

- benefits are not calculated from it;

- no pension contributions are made, that is, no pension is generated;

- the employee is deprived of social guarantees established by law;

- the risk of being left without earnings and without work increases;

- lack of state assistance in the event of a conflict situation.

Procedure and terms of accrual and payment

Employees are paid in accordance with the Labor Code of the Russian Federation. The amount of earnings is established by an employment agreement with the employee, additional payments are recorded in local acts enterprises. Employees are introduced to them when they are employed or when changes are made to the documents concerning their earnings. Staff salaries are calculated on the basis of primary documents.

The main ones are:

- time sheet;

- orders for personnel (on admission, dismissal, vacations, etc.);

- orders on bonuses;

- disability certificates;

- holiday work orders, etc.

The main payments due to the employee under the contract are entered into the program when he is accepted. The rest of the surcharges are added to the base within a month on the basis of the corresponding securities. The documents, as they are received by the accounting department, are entered by the calculator into the salary program.

In some regions, the authorities have established district coefficients and other allowances, which are also taken into account in the calculation.

Earnings are paid twice a month. The first payment is an advance payment. It is no more than 50% of the basic income. If the employee did not work for the first 15 days of the month, the advance payment is not charged to him. If part of a half of the month has been worked, it is calculated in proportion to the time worked.

The calculation of earnings is made in the payroll, it is issued on payment. There is a universal document that groups calculation and payment - this is a payroll.

Personal income tax is withheld from the salary accrued for the period of each worker in the amount of 13%. The amounts of deductions established by law are not taxed (Article 218 of the Tax Code). They are provided to some employees on the basis of supporting papers.

For example, if there is a minor child or full-time student in the family, each of his parents is provided with a standard deduction in the amount of 1,400 rubles each month. For its registration, an employee's statement and a copy of the child's birth document are required.

The employer is obliged to pay the basic earnings by the 15th day of the coming month for the settlement month, and the advance payment - 15 days before that. The company sets specific payment dates independently and fixes them in local documents.

An example of the calculation of earnings and taxes for May 2017. An employee has two minor children.

Initial data for calculating earnings:

- salary - 40 thousand rubles;

- monthly payment for seniority - 15% of the salary;

- vacation from May 10 to 14, 8 thousand rubles were paid;

- On May 25, an advance payment was issued in the amount of 11,500 rubles.

Earnings are accrued in the following order:

| Determination of hours worked according to the timesheet | In May 20 working days, the employee worked 15 (20 - 5 days of illness). |

| Calculation of charges |

Total: 30,000 + 4,500 + 8,000 = 42,500 rubles. - accrued in May. Calculation of deductions. Personal income tax: (42,500 - 1,400 - 1,400) * 13% = 5,161. |

| Amount to be issued | 42,500 - 11,500 - 5,161 = 25,839 p. |

| Taxes paid by the company on employee earnings | 42,500 * 30.2% = 12,835 rubles, of which insurance contributions:

The company is obliged to transfer personal income tax from earnings to the budget on the day of salary payment or the next, and from sick leave and holidays - until the end of the month. Insurance premiums must be transferred by the 15th day of the month following the calculated one. If the limit date coincides with a weekend or holiday, it is postponed to the next weekday. Failure to pay or delay in earnings is punishable by fines. Also, the employer must pay each employee compensation equal to 1/150 of the key rate of the Central Bank of the outstanding amount for the day of delay. |

What taxes are paid

In Russia, income tax is personal income tax, which for the bulk of Russians is 13%. There are contributions to off-budget funds - 30.2%. They are paid by the employer from the wage fund (payroll).

The corresponding percentages in force in 2017 are shown in the table:

The percentage of contributions “for injuries” can be higher than 0.2%. Its value depends on the type of activity of the company and is established by social insurance during the registration of the policyholder. The higher the risk of injury at work, the higher the percentage of deductions.

Example. The organization employs five people. The salary of each is 10 thousand rubles. per month. For April 2017, the employer will withhold personal income tax from each worker in the amount of 1,300 rubles. With payroll equal to 50 thousand rubles. the company will pay the fees 15,100 rubles.

An entrepreneur who does not have employees for 2017 must pay contributions of 27,990 rubles, of which 23,400 (26% of the minimum wage per year) - for pension insurance and 4,590 (5.1%) - for medical insurance.

If the individual entrepreneur's annual income exceeds 300 thousand rubles, he is obliged to transfer an additional personal contribution to the Pension Fund. It is 1% of the amount exceeding the specified limit. The amount for pension insurance transferred by individual entrepreneurs per year should not exceed 8 minimum wages.

For non-payment of taxes in fixed time penalties are provided in the amount of 1/300 of the Central Bank discount rate per day of delay.

So, the salary at the enterprise must be calculated and paid in accordance with labor legislation. The procedure, rules, amounts of charges, the conditions for their provision are fixed in the local acts of the company and labor agreements. Each employee has the right to know the components of his earnings. Their accountant monthly reflects in the payroll, which on the eve of payment happens to workers.

Is it obligatory to issue an order on early payment of wages in December 2017? What does a sample of such an order look like and what should be written in it? How long does it take to publish it? Do I need to introduce employees to him? From the article you will find out the answers to these questions and you can download the completed sample order.

Early payment of wages in December: is it possible or not

Is it possible to pay wages for the second half of December 2017 before the New Year and is it necessary to issue an order for this purpose? This is a question that many accountants may face before the start of 2018. Let's take a look at the legislation.

So, wages should be paid at least every fortnight. The exact date of payment of wages must be spelled out in the internal labor regulations, collective or labor agreement - no later than 15 calendar days from the date of the end of the period for which it was charged. This is provided for by article 136 of the Labor Code of the Russian Federation.

However, in many organizations, the second part of the salary payment for December does not fall on a weekend (for example, it falls on January 10, 2018). Can this part of the salary be paid ahead of schedule in December? There are different opinions on this matter.

Opinion 1: the salary for December before the new year cannot be paid

If the deadline for the payment of the salary falls on January 10, 2018 (Wednesday), then you must also pay the salary on January 10. It is impossible to issue wages earlier, since Article 136 of the Labor Code of the Russian Federation requires the determination of a specific date for payment of wages.

Opinion 2: the salary for December can be paid ahead of schedule

Article 136 of the Labor Code of the Russian Federation provides that wages should be paid "at least every half a month." Thus, the law establishes "at least". But you don't have to pay exactly twice. You can pay three or more times. There are no prohibitions on this in Labor Code RF is not.

Our conclusion

In our opinion, the employer has the right to pay wages for December ahead of schedule. This does not violate workers' rights in any way. In this regard, the salary can be issued not in January, but, for example, in the period from 25 to 29 December 2017. However, we believe that the most logical during this period is not to issue the final payment for December 2017, but to make another interim payment - an "unscheduled advance". And in January 2018 (on time, documented) it will be possible to make the final calculation, pay the "balances" and withhold personal income tax.

The employer does not face a fine for the payment of wages ahead of time. It doesn't matter for what reason the organization violated the regularity of payments - in connection with the upcoming weekends and holidays, or just like that. This opinion is shared by the Ministry of Labor in a letter dated December 6, 2016 No. 14-1 / B-1226.

Example.

Salary Petrenko N.V. is 30,000 rubles. Labor contract it is established that the advance is paid on the 25th, and the second part of the salary - on the 10th. December 25, 2017 Petrenko N.V. paid an advance payment for December in the amount of 15,000 rubles. The employer, on his own initiative, wants to pay the employee the salary for December ahead of schedule - December 29, 2017. On this day Petrenko N.V. will transfer one more "interim advance" in the amount of 14,500 rubles. Another 500 rubles (final payment) will be transferred to the employee on January 10, 2018. Thus, by January 10, 2018 Petrenko N.V. will receive his full salary: 30,000 rubles (15,000 + 14,500 + 500). Moreover, the employee will receive most of it before the New Year.

In principle, it is possible to make the final calculation for December 2017 in December, but not very logical. Moreover, this may require recalculations from the accountant in the future. The fact is that logic is lost - the month is not over yet, and the accountant has already drawn up a timesheet and calculated the salary. In our opinion, this should not be done.

Preparing an order for early payment of wages in December

Pursuant to article 9 Federal law from 06.12. 2011 № 402-FZ "On accounting" each fact of economic life is subject to registration of a primary accounting document. Accordingly, the employer must necessarily have in place some administrative document on early payment of wages in December 2017. For these purposes, an appropriate order may well be suitable. Here are some examples of such an order.

Order for early payment in December of interim advance: sample

Suppose that the accountant has chosen the option where the interim advance for December will be paid in December 2017. And the final payroll will be made in January 2018.

Of course, it is advisable to prepare the order in advance so that the accountant has time to carry out all the calculations and prepare them for payment through the bank. In the order, in our opinion, it is logical to stipulate at least:

- reason for early payment;

- term of early payment;

- instruction on the deadline for the final settlement for December.

Let us give sample sample order for early payment of wages in December 2017. Such a document is needed, first of all, for the accounting department in order to correctly make calculations.

December full early pay order: sample

As we have already said, no one prohibits the employer from paying full wages to employees in December 2017. This will also require an administrative document (order or order of the head). However, in this case, the order will be slightly different. After all, it will need to write about the full payment of the December salary. Here is a sample completed sample.

In our opinion, it is not necessary to acquaint all employees with the order for early payment of wages, since such an order most likely does not violate the rights of workers who will simply receive part of their wages (or in full) earlier.

Some workers may not agree with early payment of wages in December. There may be such! And, indeed, they may be right if they wish to receive salaries for December exactly on the date specified in the labor agreement, collective agreement or labor regulations. Such workers, of course, need to meet halfway!

On the market software products there are often suggestions "we make programs to order", well, or the like, for the Buchsoft Salary program no special programmer is required. BukhSoft program - ready-made solution, which either already meets your requirements, or requires little effort, so that the specifics of your requirements would be taken into account in the program as soon as possible.

Write to us about your wishes, and we will tell you where this is already provided for in the program!

It's easier to start working in the program than in Excel!

Here are the steps that allow the program to calculate salaries, calculate all taxes (personal income tax and insurance premiums) and get everything required documents:

- Download and install the program

- In the Organization Details, enter the name and personal injury premium rate (all other details can be entered later)

- In HR data, enter your full name, date of birth and standard deductions, if any (the rest of your HR data can be entered later)

- In the payroll calculation, click on the Accrue button (for all employees or for each).

As a result, you will automatically have correctly calculated all taxes from the payroll fund and filled in all the necessary documents for calculating salaries.

Here are some of the documents that the salary program automatically fills in:

Automatic payroll calculation based on personnel data and timesheet

Of course, over time, it becomes necessary to demand even more automation from the program.

The convenience of the program lies in the fact that when you enter permanent accruals in personnel data, the calculation of salaries, deductions, taxes from salaries is performed in one action for the entire list of employees (the "List" button). At the same time, if the accrual relates to salary payments and the user maintains a timesheet, then the program automatically takes into account only the days worked. If the user does not maintain a time sheet, then the salary is charged in full. Also, according to personnel data, the accrual of sick leave and vacation pay is automatically tracked. Thus, in the presence of initial information on the calculation of wages, the entire procedure for calculating wages and the formation of required documents produced in automatic mode in a few minutes even in large enterprises.

If necessary, the program has the ability to make individual payments through the employee's personal account.

Wide range of customized payroll charges

The program automatically calculates almost all known charges. For each charge to the program, settings have already been made, how exactly taxes should be calculated from it.

Here are some of the types of charges provided in the program:

- salary payment, piecework payment;

- permanent and one-time bonuses, allowances and surcharges;

- royalties;

- remuneration under a civil law contract;

- temporary disability benefit and other benefits;

- payment of annual (additional) vacations;

- compensation payments;

- accruals for regional coefficients;

- dividends;

For all charges, settings were made to calculate the corresponding taxes and contributions.

If necessary, the user can add any of his own accrual and customize the calculation of taxes.

One of the advantages of the "BuchSoft: Salary" program is that it provides for the automatic generation of income statements individuals(employees) in the form of 2-NDFL. At the end of the year, when the salary for all months has been calculated, the program will generate a file and copy it to a USB flash drive in full compliance with the requirements set by the tax authorities.

We wish you pleasant work!

Fujifilm X-T1 - Full Review

Fujifilm X-T1 - Full Review Lenses sony sel. Sony lenses rating. Which Sony lens to buy

Lenses sony sel. Sony lenses rating. Which Sony lens to buy Canon PowerShot Pro1 - quality that ends quickly Canon PowerShot G5 X highlights

Canon PowerShot Pro1 - quality that ends quickly Canon PowerShot G5 X highlights